As the world enters the Age of Electricity, lighting remains one of the most visible – and widespread – parts of our energy use.

The IEA estimates that lighting in buildings and outdoor applications accounts for the majority of overall lighting electricity demand. In 2024, around 8% of global electricity demand – or about 2 200 terawatt hours (TWh) – was attributed to lighting in buildings and outdoor applications, excluding industry and agriculture. These figures reflect the latest available data and define the scope of the analysis presented in this commentary. Estimates from industry and experts1 place global electricity consumption for lighting, including industrial lighting, between 2 500 and 3 500 TWh in recent years.

Over the past two decades, lighting has seen major efficiency gains thanks to the rapid uptake of the light-emitting diode (LED). A typical halogen lamp produces about 20 lumens per watt2 (lm/W), while a compact fluorescent lamp (CFL) reaches around 50 lm/W. Meanwhile, LEDs sold today average close to 100 lm/W – with some premium and professional LEDs exceeding 200 lm/W. Supported by strong policies and innovation, LEDs have become one of the biggest energy efficiency success stories of recent years, with long lifetimes and falling costs helping them dominate global markets. The efficiency gains have contributed to improved energy security, reduced energy bills and avoided higher emissions.

Yet the global LED transformation is not over, and a second wave of deployment is now taking shape. Uptake remains uneven across regions, while demand for brighter spaces and illuminated infrastructure continues to rise around the world. Moreover, the first generation of already-installed LEDs is approaching end-of-life, creating an opportunity for the next phase of LED adoption – one that is focused on higher performance, longer lifetimes and smarter systems.

Global LED adoption is moving at three speeds

The global shift to LEDs has been strongly supported by government policies. Minimum Energy Performance Standards (MEPS) – which now cover about 110 countries – and labelling schemes have been key drivers. Energy efficiency obligation schemes, such as white certificates and renovation programs, have also helped stimulate LED adoption. In addition, international agreements such as the Minamata Convention on Mercury, with more than 150 Parties, are further accelerating the shift away from fluorescent lighting. China is currently the world’s dominant producer of fluorescent lamps and has recently approved measures in line with the Convention, which will also help shift production and exports towards mercury-free LED alternatives.

Within this global policy landscape, three distinct regional adoption patterns have emerged:

- Front-runners: China and India currently lead global LED adoption, with market shares exceeding 85% and 75%, respectively. This success has been largely driven by supportive regulation and large-scale public programmes. In India, bulk procurement schemes under the UJALA programme have sharply reduced LED prices and enabled nationwide mass replacement of existing lamps, notably in households and street lighting. In China, mandatory standards, labels and rapid urban retrofits have played a similar role in widespread LED uptake.

- Strong adopters: Europe and North America also show high policy support and strong market uptake, but lamp replacement rates have been slower and stock shares are 10-20% lower than in China and India. These continents already relied heavily on efficient CFLs and improved halogen lighting before LEDs became cost-competitive, reducing the immediate incentive to switch.

- Catching up: Across much of Africa, Southeast Asia and Latin America, LED sales shares now range from 50% to 85%, although policy coverage remains uneven. Regional initiatives in Southern and Eastern Africa and ASEAN show how coordinated standards can accelerate progress. Parts of Latin America - including Argentina, Brazil, Bolivia and Chile - as well as the United Arab Emirates, were early movers in eliminating incandescent lamp sales or banning their imports.

Lighting in buildings offer a potential route to further efficiency gains

Built floor area worldwide has grown by over 20% over the past decade, but electricity use for lighting in the buildings sector has been relatively stable, largely due to the rapid spread of highly efficient lighting technologies. As a result, lighting’s share of buildings’ total electricity consumption has fallen as demand grew in other end-uses such as space cooling and data centres, driven by economic and demographic growth. Lighting is now the only major building end use where efficiency gains have largely offset growth in floor area and population.

Today, the services sector represents the majority of lighting energy demand in buildings. LEDs are common in new buildings, but retrofits are often delayed as they can be complex – for example, due to issues with ceiling access, rewiring or installing new fixtures. They are therefore typically carried out alongside major renovation and refurbishment activities, rather than as standalone lighting interventions. In the European Union, for example, National Buildings Renovation Plans can support lighting renovations by making energy-efficient upgrades to buildings part of national climate and energy strategies.

Residential lighting has the highest LED adoption rate across sectors. Replacements in households are driven mainly by end-of-life considerations, as people tend to delay replacing older bulbs until they fail – with affordability and product availability shaping choices.

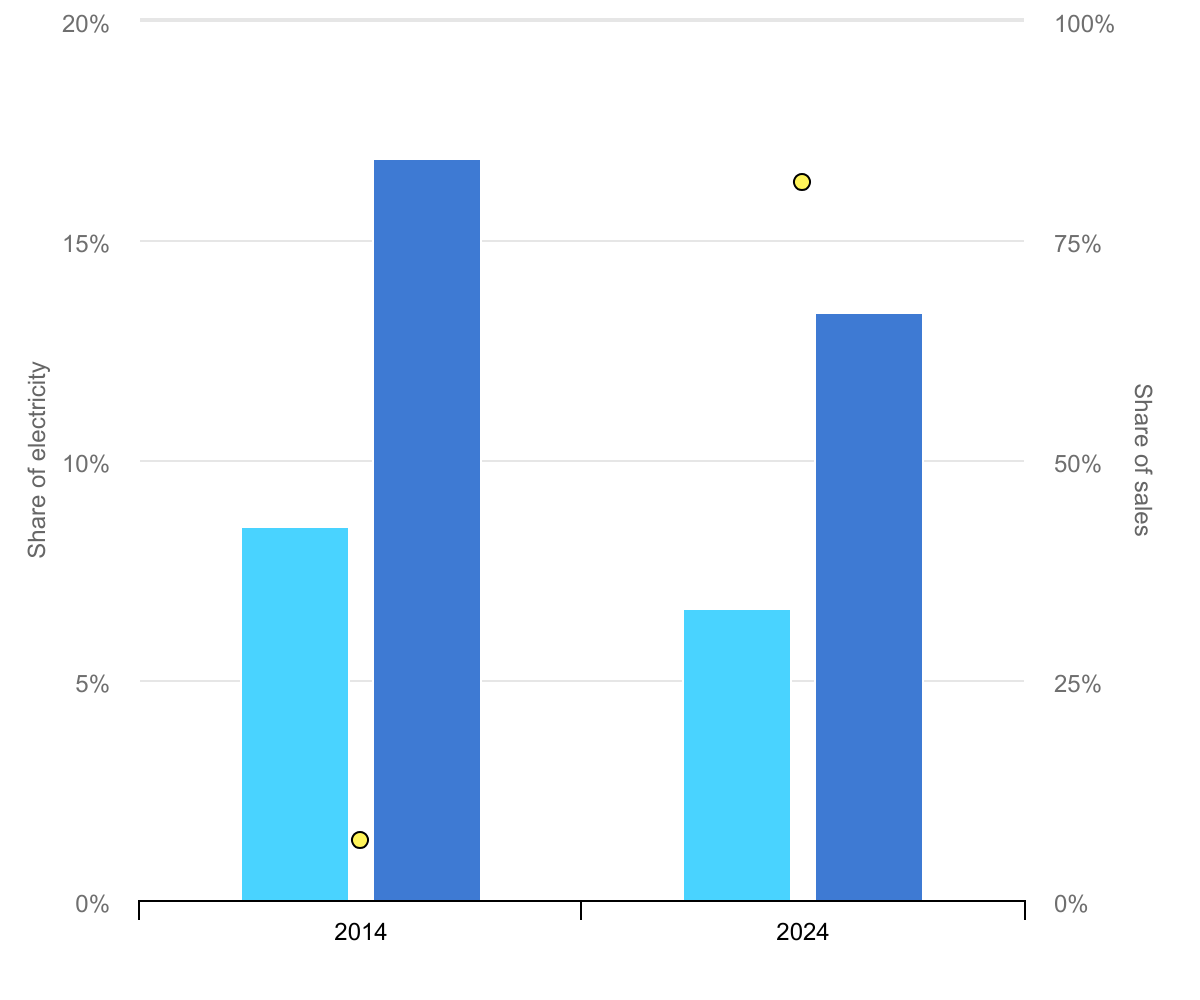

Share of indoor lighting in buildings in electricity demand, 2014 and 2024

Share of electricityShare of sales2014 and 2024

- In final electricity demand

- In buildings electricity consumption

- LEDs average market share

Sources

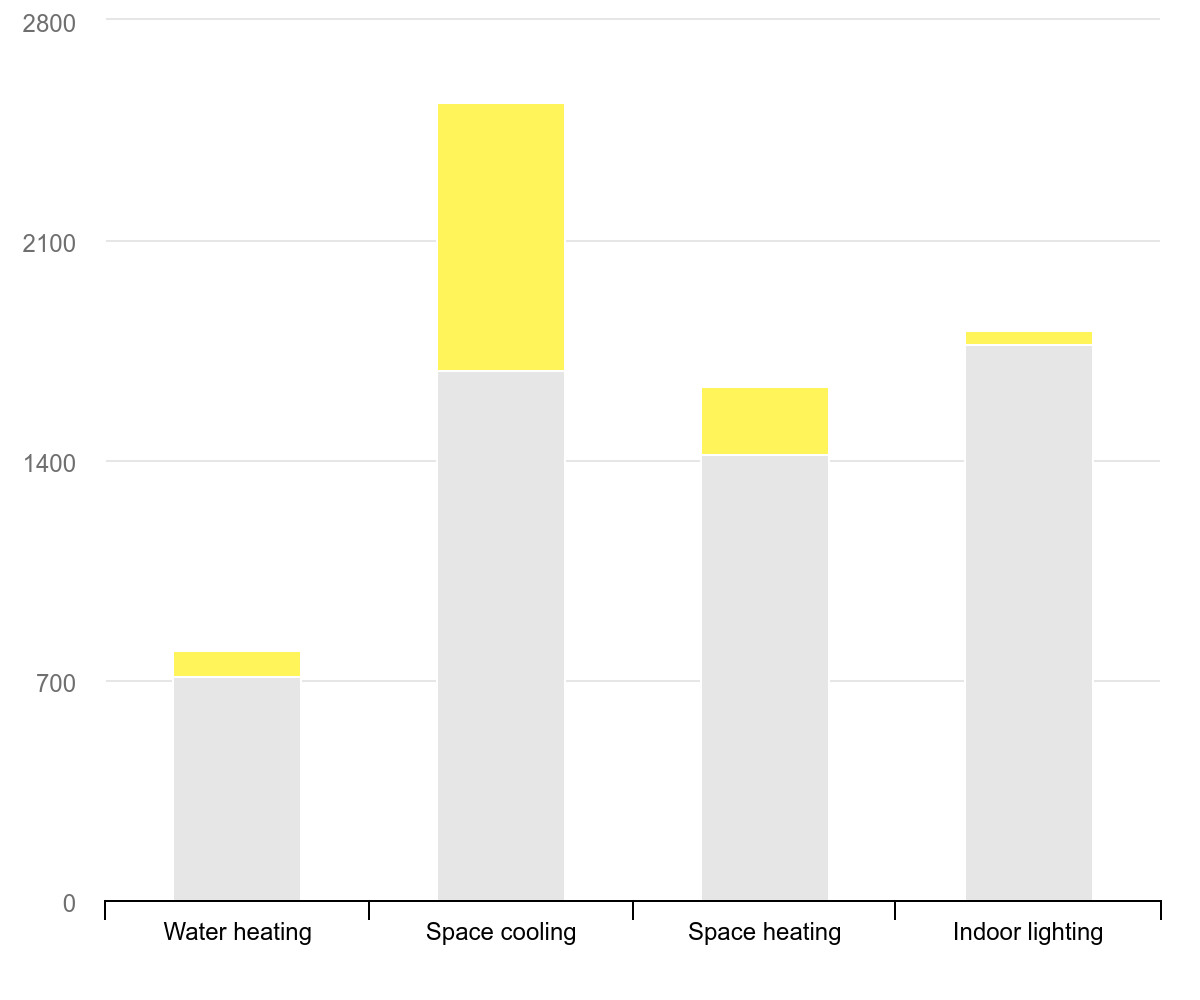

Electricity consumption of selected end-uses in buildings, 2014 and 2024

TWh

TWh

Water heatingSpace coolingSpace heatingIndoor lighting0700140021002800

- 2014

- 2014-2024 growth

These improvements in lighting have already avoided substantial electricity demand in buildings. If lighting technology efficacies (lm/W) and market shares had remained constant worldwide over the past decade, annual residential lighting electricity consumption would be more than 500 TWh higher today – roughly equivalent to the total electricity demand of South Korea. Similarly, in the services sector, indoor lighting electricity consumption would be about 800 TWh higher – exceeding total electricity consumption across Africa. Combined, this would imply around 70% higher electricity consumption for indoor lighting in buildings.

Further improvements are easily achievable. The average LED efficacy has roughly doubled since 2015, and best-available products now reach up to 230 lm/W — nearly twelve times the efficiency of halogen lamps. Yet many buildings still rely on mid-range products installed years ago, leaving substantial efficiency potential untapped. At the same time, more intensive lighting use and more lamps per square metre may offset some gains.

In all sectors, LEDs offer efficiency opportunities while supporting broader electrification

Lighting continues to offer opportunities for efficiency gains in all sectors, freeing up electricity for other uses and supporting broader electrification. Two areas stand out for further efficiency improvements:

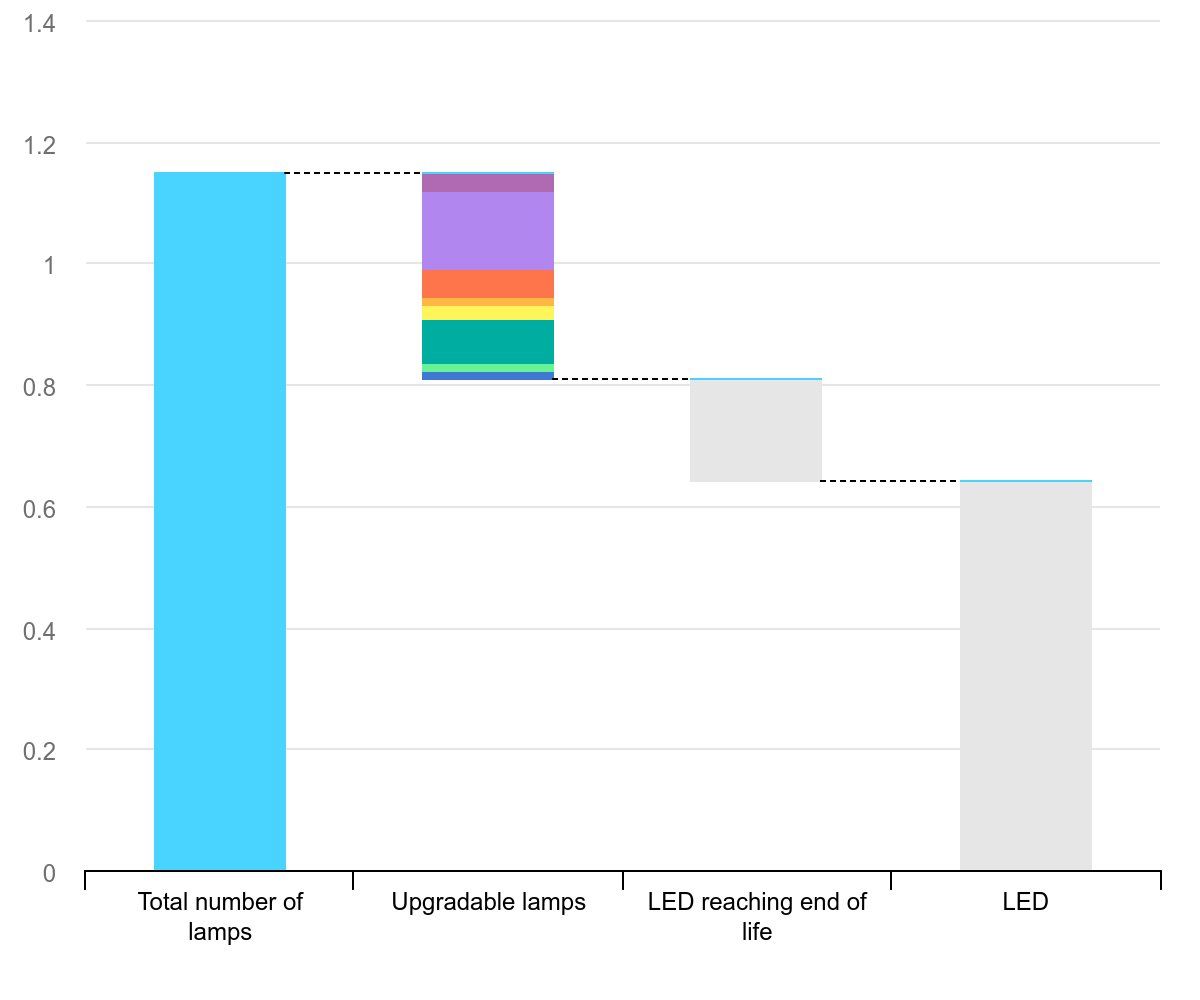

- Low penetration in many emerging economies: Across much of Africa, Central and South America and Asia-Pacific (excluding India and China), there is still relatively low LED penetration. In the residential sector alone, 30% of lamps globally have yet to be upgraded. This creates an opportunity to leapfrog directly to high-efficiency LED technologies.

- End-of-life replacement for early-generation LEDs: Early-generation LEDs with 10–15 year lifetimes are reaching end of life. Nearly 15% of residential lamps now fall into this category, creating an opportunity to replace them with more efficient – and potentially smarter –systems.

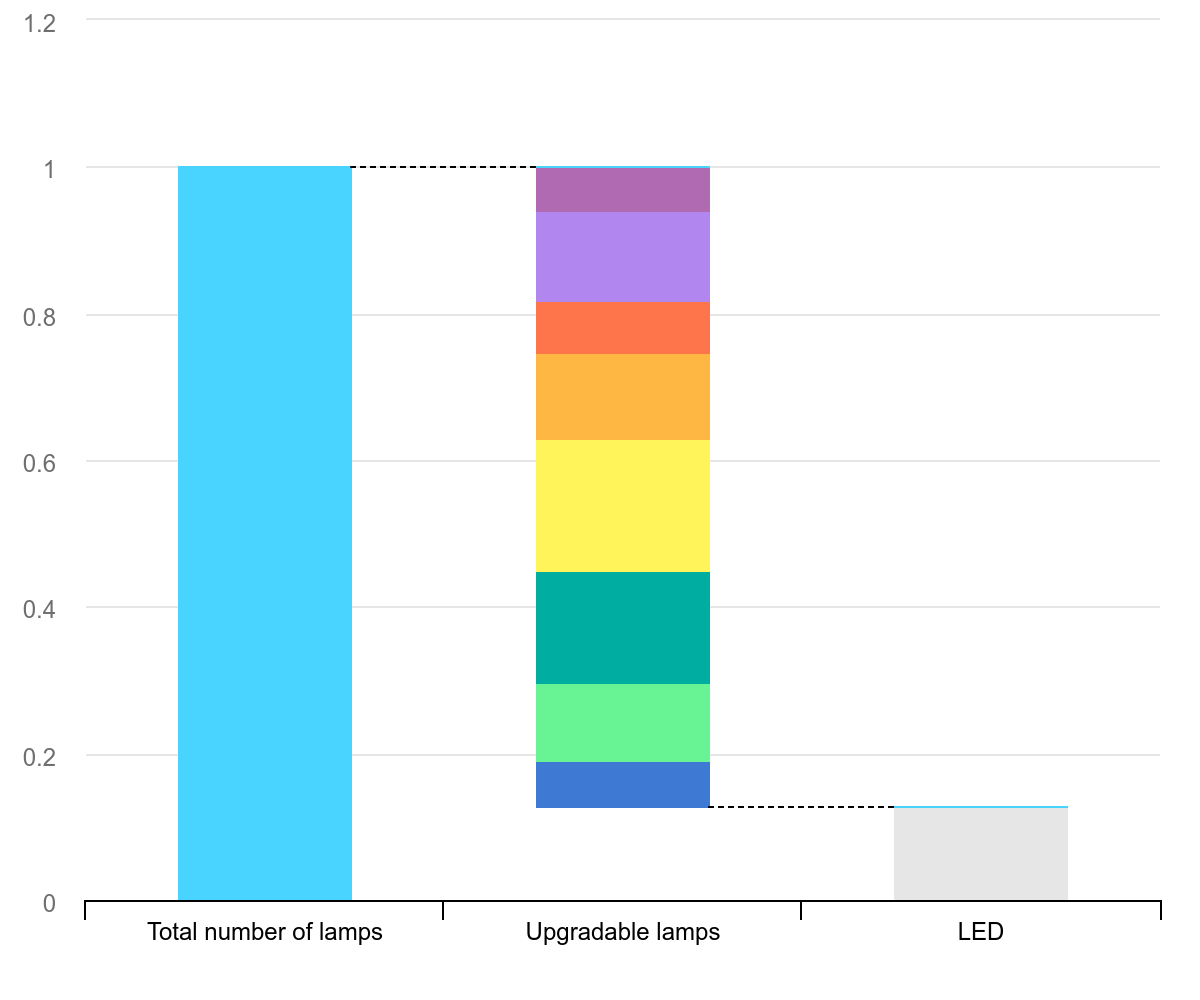

Total stock of residential lamps that are upgradable to LED or approaching end of life, per region, 2014

Index (1 = number of lamps in 2014)

Total number of lampsUpgradable lampsLED

- World

- North America

- Europe

- Other Asia Pacific

- China

- India

- Central & South America

- Africa

- Rest of World

- LED

Total stock of residential lamps that are upgradable to LED or approaching end of life, per region, 2024

Index (1 = number of lamps in 2014)

Total number of lamps Upgradable lamps LED reaching end of life LED

- World

- North America

- Europe

- Other Asia Pacific

- China

- India

- Central & South America

- Africa

- Rest of World

- LED

Outdoor public lighting also offers additional opportunities for LED upgrades, often with fast payback – particularly through coordinated street light retrofits. However, fragmented ownership, legacy fixtures and limited procurement and institutional capacity continue to slow LED deployment.

Other privately owned outdoor lighting may also lack centralised programmes. Barriers are mainly related to up-front costs or design constraints, such as older fixtures, shielding and optics.

Capturing the next phase of LED efficiency gains will depend on design, performance and cost

Capturing the next wave of lighting efficiency improvements depends on three principles:

- Design for longevity and circularity: Efficiency alone is no longer sufficient; upgradability and circularity are increasingly important for enabling widespread LED efficiency gains. Modular lighting systems that allow individual components such as drivers, optics, and control units to be replaced can reduce waste and lifecycle costs. Reparability can also extend product lifetimes, while reconditioning and reuse (for example, cleaning, polishing and component replacement) can lower material demand. Recycling also remains important for LED supply-chain resilience, for example in the context of the EU Circular Economy Act targets for lighting products. Efficiency gains should not be offset by more complex, vendor-locked systems that rely on non-standard components or embedded software, which limits interoperability and repair. Some products – such as adhesive LED strips – are especially difficult to repair or recycle, raising circularity concerns.

- Improve system-level performance: Lamp efficacy is only part of the story. Controls such as occupancy and daylight sensors – which are already mature and cost-effective – can deliver significant additional savings, particularly in non-residential buildings. Integration with building management platforms can enable predictive maintenance, adaptive and motion-responsive lighting and detailed usage analytics. Direct current (DC) systems – where LED lights operate using DC electricity rather than conventional alternating current – can further reduce energy conversion losses in buildings with on-site renewables. However, fragmented smart-lighting protocols risk limiting benefits. Unlike other consumer electronics, most smart lightbulbs are still tied to proprietary hubs.

- Enable widespread adoption: Affordability remains a key barrier to LED expansion. Although LED prices have fallen sharply in recent decades, best-in-class products with advanced controls can still cost several times more than basic models. In low-income regions, high upfront costs can slow adoption despite significant lifetime savings. In other markets, low or subsidised electricity prices weaken the investment signal. New business models – including low-interest financing and Lighting-as-a-Service – can help lower financial barriers. At the same time, performance standards should continue to tighten to ensure that efficiency improvements reach the market.

- Global cooperation through initiatives such as the just-launched ELECT Project in Zambia and the longstanding IEA 4E Technology Collaboration Programme supports the diffusion of best practices and performance benchmarks. The Smart Sustainability in Lighting and Controls Platform – one of the IEA 4E initiatives – brings together global stakeholders to develop information that can improve efficiency in lighting markets. Finally, broader flagship projects that combine smart technology, circular design and innovative finance can demonstrate what is possible and accelerate wider market adoption in municipal and building-level projects.

Sophie Attali of the IEA; Kevin Lane, Michael Scholand and Georges Zissis of the IEA 4E TCP; and Paolo Ceccherini and Deepak Joshi of Signify contributed to this commentary.

Post time: Apr-15-2026